How to Get out of Debt the Smart Way

It's hard to get excited about waking up in the morning and going to work to pay for a thrill you've already had.

But it's always best to get out of debt as quickly as possible.

This eliminates a huge source of financial stress and allows you to focus on building a better financial future for you and your family.

There is no rocket science to debt reduction. If you want to pay your debt off faster, the smartest and most obvious strategies are:

Increase the regular repayment amount

Decrease the interest rate

Sell some non-essential items and make lump sum debt reductions

Stop digging the hole deeper (cut up the cards)

If you have more than one debt you need to add the following to the list above:

Increase the repayments on your highest interest rate debt in preference to your lower interest rate debts

Prioritise paying off non-tax-deductible debt over tax-deductible debt which may give you the benefit of paying less tax

It can get complicated if you have to choose between options that are not so clear. For example, do you focus on paying off a non-tax-deductible debt when it isn't the highest interest rate debt?

If you have complexities, I recommend you talk to your mortgage broker and accountant and get them to work together on your most effective debt reduction plan.

If you don't have anyone you normally trust with stuff like this, shoot me an e-mail and I'll give you some options.

Today let's keep it simple.

Refinancing a Mortgage

A mortgage is a debt that many of us will decide is right for us.

Although mortgages are considered “good debts” because you're paying for a valuable and appreciating asset, you still have to make the payments and, ideally, you don't want to pay any more than you need to.

If you have a mortgage and have not reviewed it in the last 12 months you can probably refinance to a lower interest rate.

Here are the pros and cons:

Pros: A lower rate can mean lower repayments or a shorter loan timeframe.

Cons: Sometimes the costs involved can cancel out the benefit. Don't forget: add the cost for swapping banks to the new loan.

Traps: If you have just spent 5 years paying off a 20 yr mortgage and are offered a new 20 yr mortgage with lower repayments there is no magic in that. You just extended your original loan out to a 25 yr loan so of course repayments will be lower!

Tips: If you refinance the mortgage to a lower interest rate, make the same repayments you were making on the previous loan. You will get ahead on your payments and get out of debt faster.

Currently, interests rates of 4% are possible for home loans. How much are you paying?

If you would like to work out if there really would be a benefit in renegotiating your mortgage, I created a simple online excel based calculator just for today's message, so make use of it. CLICK HERE to go to the calculator.

There is one box in that calculator where you are required to enter the cost of refinancing. Brokers suggest that $750 is a reasonable estimate to enter there for a standard bank swap, but if you want to get a more accurate figure you will have to make some phone calls or enquire/search online.

Also, if you have a fixed interest rate with your current bank there may well be other charges too, so you will need to find out and add those as well.

You need to know how many months you have been paying off your current loan and what the current balance is.

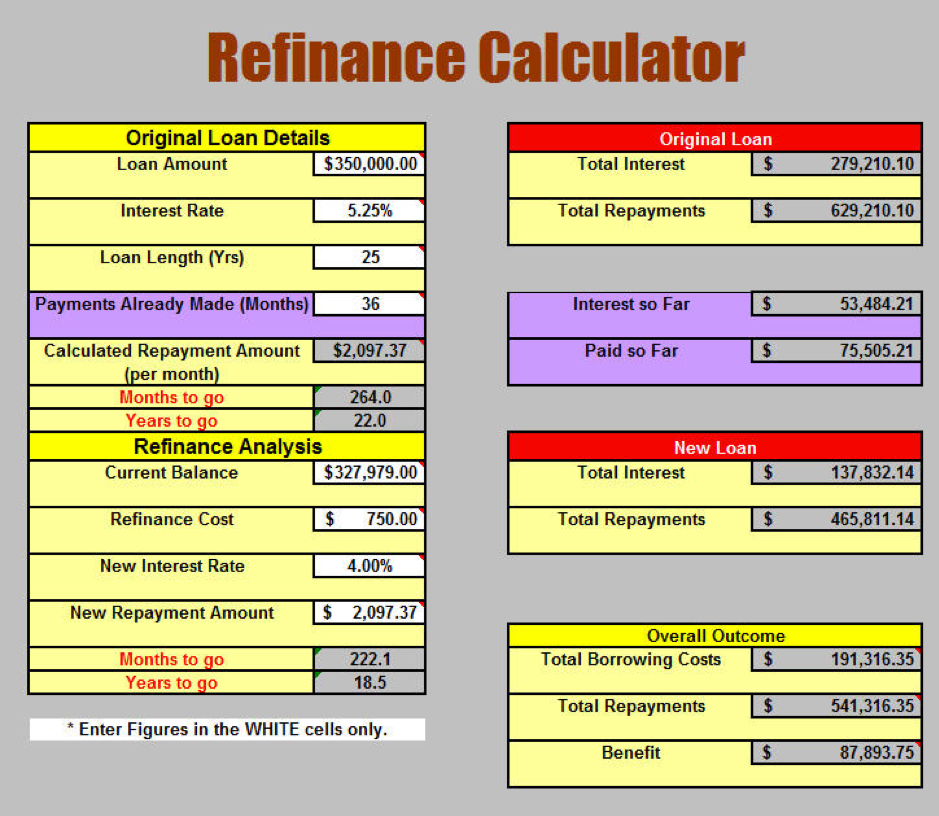

Here is an example of what it can do.

Here we can see a $350,000 mortgage that has been going for 3 years at 5.25%.

Currently, it still has 22 years to go. If we refinance the mortgage to 4% that comes down to 18 ½ years if the repayment is maintained at the same level as at 5.25%.

That saves a massive $87,893.75 in interest!

I encourage you to experiment with the ‘New Repayment Amount' and see what impact a few dollars extra can make.

Here are some other things to consider:

If you don't have a mortgage but you do have unsecured debts such as Credit Card debt, look at options to refinance that to a lower interest rate. Maybe a personal loan with a Credit Union would be an option for you to look into. (The calculator will work for that scenario as well.)

If you feel you can't deal with your finances right now and/or you are tired of money stress and have decided it's time to take control, talk to a Spending Planner to find out how you can break the cycle - BOOK A FREE CALL

You have nothing to lose and lots to gain. Spending Planners are non-judgmental professionals who are trained to help. A short relationship with a Spending Planner will provide you with tools and training that will benefit you for the rest of your life!

To find out more about becoming a Spending Planner, CLICK HERE

Creating your own personal Spending Plan will be one of the best things you ever did.

Request a Call From The Spending Planners Institute 1300 918 450